Getting Started - An Operational Framework For Disaster Risk Finance

Tying together the experience and collected knowledge from partners in the public and private sector, this section creates a practical operational framework for governments looking to establish or improve disaster risk financing and insurance programs. As a framework for the development and implementation of cost-effective and sustainable solutions it aims to provide a practical approach and a comprehensive overview of policies for the public financial management of disasters by governments.

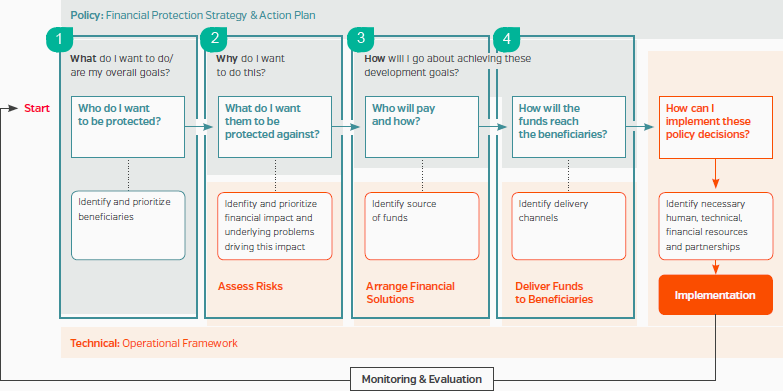

This operational disaster risk financing and insurance framework provides decision makers with a practical guide for beginning relevant discussions with all stakeholders—from government agencies and taxpayers to donors and private insurance companies—and to gain an understanding of how the work might evolve over time. As a second step, it helps governments to identify and prioritize policy options and the necessary actions to implement these choices, depending on the particular situation and timeframe.

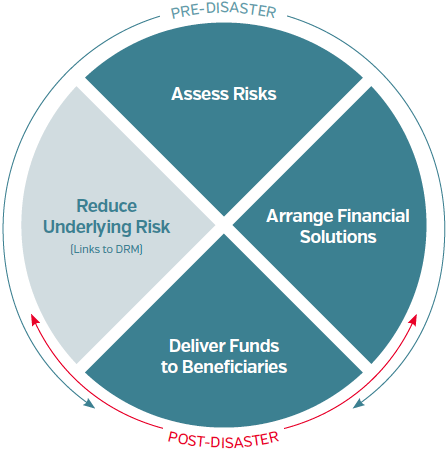

The Operational is presented in three components:

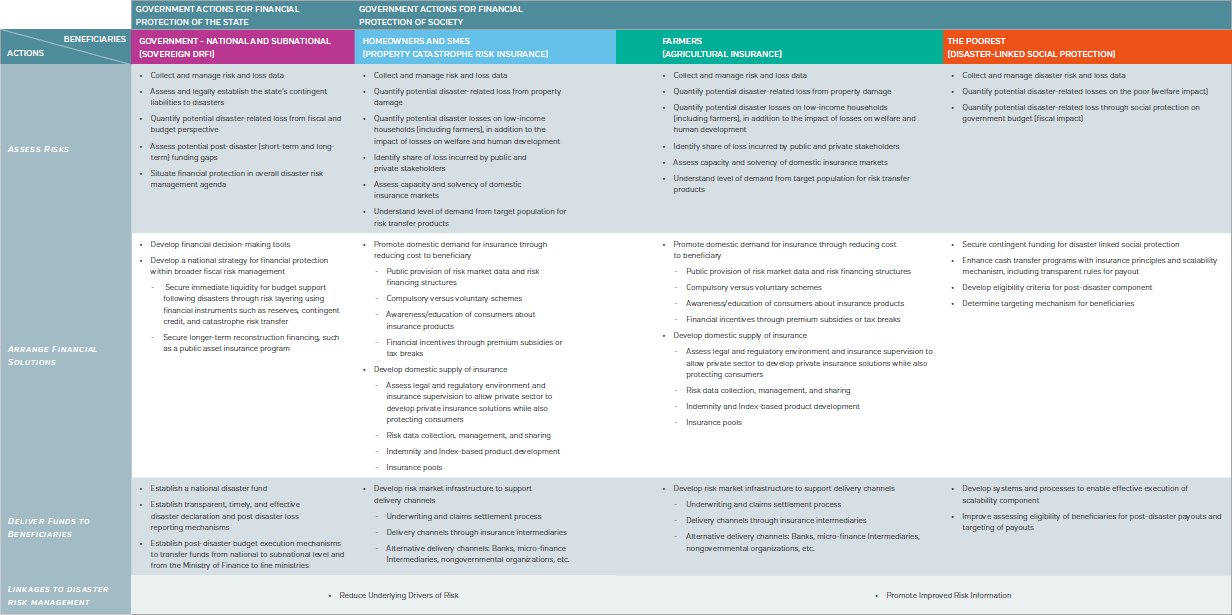

Assess Risks: Risk assessments for financial protection quantify potential disaster impacts based on historical and simulated data. This often requires investments in the necessary underlying hazard, exposure, and vulnerability data. This also includes building an effective interface between the policy maker and underlying technical models.

Reduce Underlying Risk: Sustainable financial protection requires reducing underlying drivers of this risk.

It complements risk reduction by managing residual risk which is not feasible or not cost eff ective to mitigate. It also creates incentives to invest in risk reduction and prevention by putting a price on risk and clarifying risk ownership.

Deliver Funds to Beneficiaries: Resources should reach beneficiaries in a timely, transparent, and accountable fashion. This requires effective administrative and legal systems for the appropriation and execution of funds for the government budget, insurance distribution and settlement (oft en through private channels), as well as social protection programs.

Arrange Financial Solutions: Effective post disaster response and recovery relies on access to sufficient and timely resources following a disaster.

This includes:

The second component lays out a decision process for a government interested in financial protection, with decisions to be made on both the policy and the technical side. This process seeks to first identify and prioritize the key policy objectives of the government and subsequently develop the required actions to achieve them. This decision process guides policy makers through a set of fundamental questions that determine the shape and direction of the country’s disaster risk financing and insurance engagement, embedded within an overall disaster risk management strategy

The government of Colombia, followed by Panama and the Philippines, was among the first governments to develop and publish a comprehensive disaster risk financing strategy. Engaged in identifying and managing the fiscal risk posed by natural disasters since the mid-2000s, the Risk Management Unit of the Ministry of Finance led the strategy’s preparation.

The Ministry of Finance seeks to assess, to manage, and to reduce its contingent liability related to natural disasters to support achievement of macroeconomic stability and fiscal balance.

To achieve its objective of enhancing catastrophe risk insurance for public assets over the next five to ten years, the Ministry of Finance will:

In the Philippines, the National Treasury within the Department of Finance finalized a national financial protection strategy in 2014.

Once a strategy has been developed, the government can formulate an action plan outlining specific steps it will take to implement its policy goals over the next two to three years. While the government’s longer-term strategy is likely to remain in place for five to ten years, the action plan should be a living document; the government may want to regularly review and update it, reflecting changes and developments in implementation.

Monitoring and evaluation is crucial during the strategy’s implementation to identify what works, what doesn’t work, and why, and subsequently refine the policy goals and actions. This includes both monitoring progress as well as evaluating the impact thereof and results achieved. Continuous feedback from monitoring and evaluation enables an iterative process with regular refinement and adjustments to both the strategy and action plan.

To achieve its objective of improving the financing of post-disaster funding needs at the national level, the Department of Finance will:

Select the desired option to expand Decision Tree for Disaster Risk Financing and Insurance Engagement by Governments